El modelo 347 es una declaración anual informativa de operaciones con terceras personas. Es un modelo informativo, es decir, no supone pago ni devolución de importe alguno. Es de carácter obligatorio y se presenta en el mes de febrero del ejercicio siguiente y finaliza el 28 de febrero según la Orden HAC/1148/2018, de 18 de Octubre.

Mediante este modelo se informa a la Agencia Tributaria Estatal de las operaciones que hayan superado los 3.005,06 €. Siendo éste importe la suma de todas las operaciones del ejercicio, IVA incluido, con el cliente o proveedor durante el ejercicio anterior.

El conjunto de los cuatro trimestres ha de ser superior a 3.005,06€, incluyendo el IVA.

Por lo tanto, si en el año 2018 has efectuado operaciones con algún tercero o proveedor por importe superior a 3.005,06 € en su conjunto, deberás presentar este modelo antes del 28 de febrero.

¿Qué operaciones se declaran?

Se declararán las siguientes operaciones:

- Entregas y adquisiciones de bienes, habituales o atípicas.

- Prestación y adquisición de bienes, habituales o atípicas.

- Subvenciones y ayudas no reembolsables.

- Operaciones inmobiliarias., habituales o atípicas.

- Operaciones con entidades aseguradoras.

- Anticipos de clientes y proveedores.

Obligados a presentar el modelo 347

1. Personas físicas.

2. Personas jurídicas:

- Sociedades limitadas

- Sociedades anónimas

- Asociaciones

- Colegios profesionales

3. Entidades en atribución de rentas, previsto en el artículo 35.4 de la Ley General Tributaria.

Los cuales desarrollen actividades económicas o profesionales con terceras personas por importe superior a 3.005,06€. Así como las entidades o establecimientos privados de carácter social y las comunidades de propietarios por las adquisiciones de bienes y servicios que efectúen al margen de actividad empresarial o profesional cuando su importe haya superado los 3.005,06€.

Excepciones

No estarán obligados a la presentación del modelo 347 aquellos:

1. Quienes tengan la sede de su actividad económica fuera del territorio español o no tengan presencia en España.

2. Las personas físicas y entidades en atribución de rentas en el Impuesto sobre la Renta de las Personas Físicas, por las actividades que tributen en dicho impuesto así como en el Impuesto sobre el Valor Añadido.

Por ejemplo, si siendo autónoma, un proveedor ha realizado una facturación superior a los 3.005,06€ en un año. Sin embargo, en las facturas emitidas se ha retenido el IRPF, en todas y en cada una de ellas.

3. Los obligados tributarios que no hayan realizado operaciones que en su conjunto superen la cifra de 3.005,06€ durante el año natural correspondiente o de 300,51€ durante el mismo periodo si se trata de cobro por cuenta de terceros de honorarios profesionales o derechos derivados de la propiedad intelectual, industrial o de autor.

4. Los obligados tributarios que hayan realizado exclusivamente operaciones no sometidas al deber de declaración.

5. Los obligados tributarios que deban informar sobre las operaciones incluidas en los libros de registro.

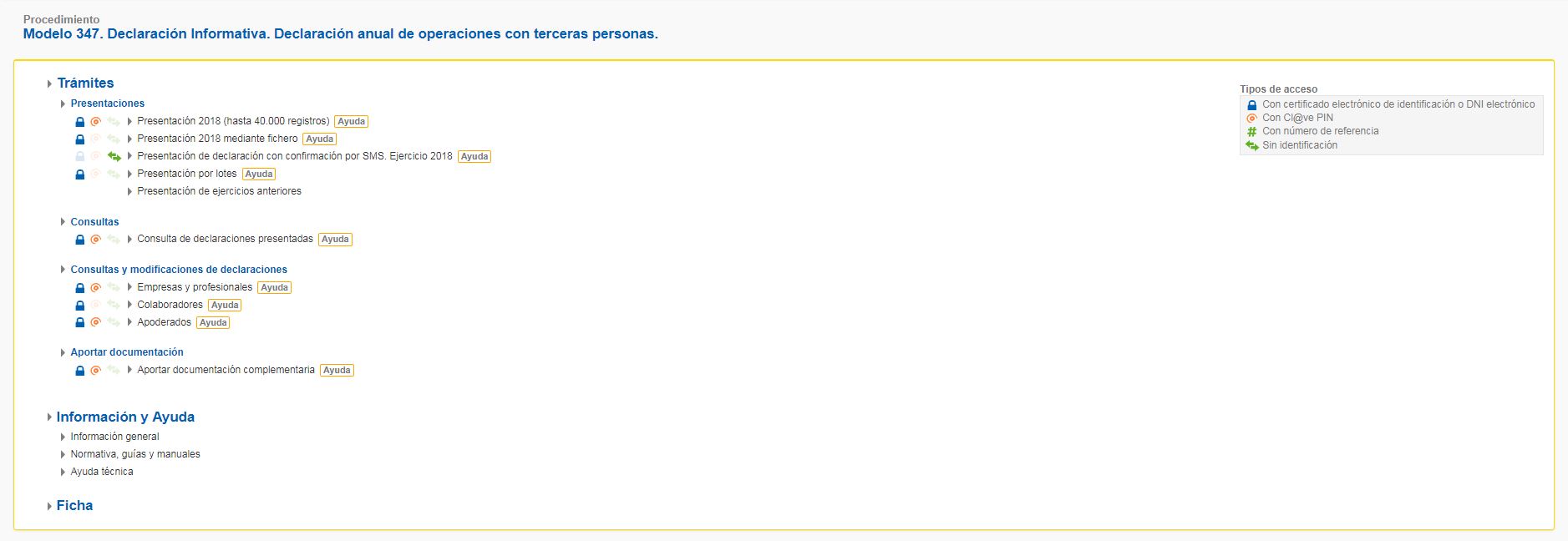

¿Cómo se presenta el modelo 347?

El procedimiento deberá ser a través de la Sede Electrónica de la Agencia Tributaria, necesitando de un certificado electrónico obligatorio para sociedades anónimas y limitadas, grandes empresas y adscritos a la Delegación Central de Grandes Contribuyentes y Administraciones Públicas o también a través de Cl@ve PIN para las personas físicas. Puedes acceder directamente aquí.

Deberás hacer clic a Presentación ejercicio 2018 para el modelo 347 e identificarte.

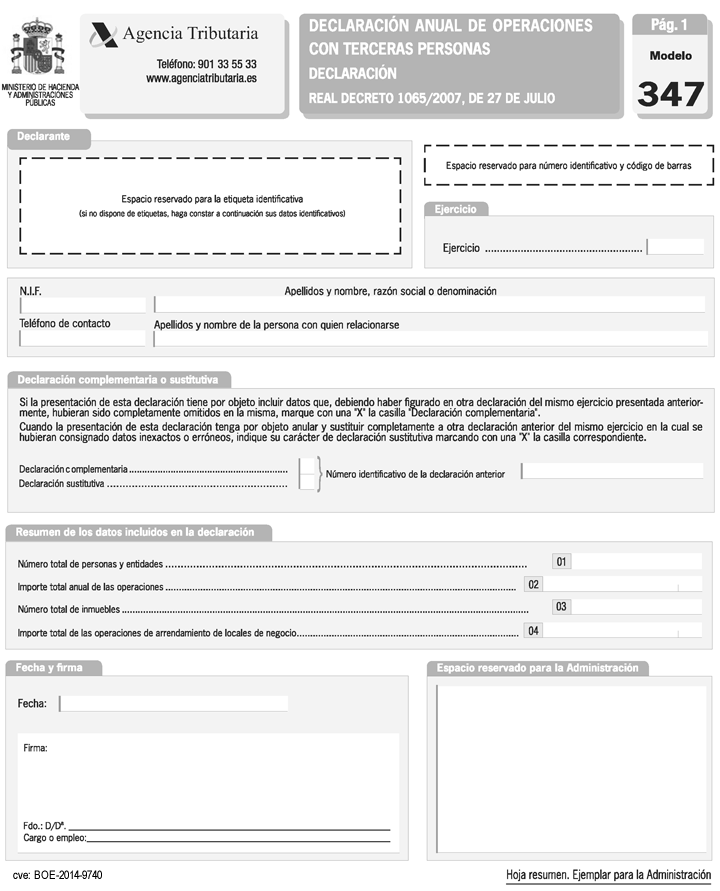

¿Cómo se rellena?

En la declaración se desglosará la información sobre estas operaciones de forma trimestral. Para cada trimestre contaremos un importe de compras o ventas contabilizando según los criterios de la Ley del IVA.

En ésta página nos identificaremos con nuestro NIF, denominación así como agregaremos el resumen de las operaciones y su importe.

En cuanto a la casilla de Declaración complementaria, se deberá marcar cuando no se hayan incluido determinadas percepciones en la declaración anterior. Por el contrario, deberás marcar Declaración sustitutiva cuando los datos sean erróneos en la declaración anterior al ejercicio.

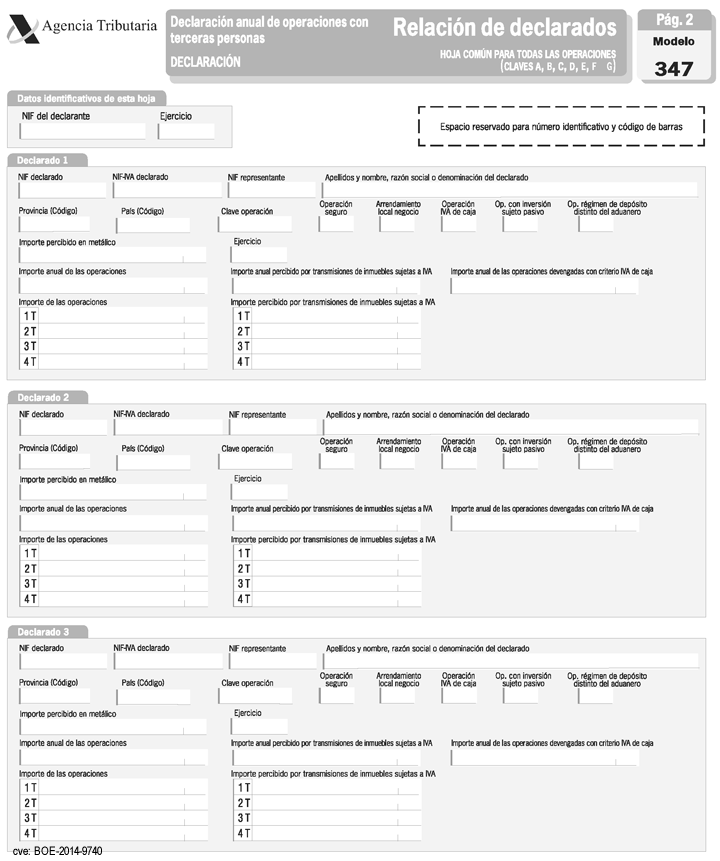

En la segunda página, además de volver a identificarnos con nuestro NIF y el ejercicio (año). Indicaremos la información de los declarados, es decir, los proveedores o clientes.

En cuanto a la clave, la mayor parte de los casos ser A o B.

- [A] Compras

- [B] Ventas

- [C] Cobros por cuenta de terceros superiores a 300,51€

- [D] Adquisiciones al margen de la actividad empresarial por Entidades Públicas

- [E] Subvenciones o ayudas (Exclusivamente para la Administración Pública)

- [F] Ventas de agencias de viaje

- [G] Compras de agencias de viaje

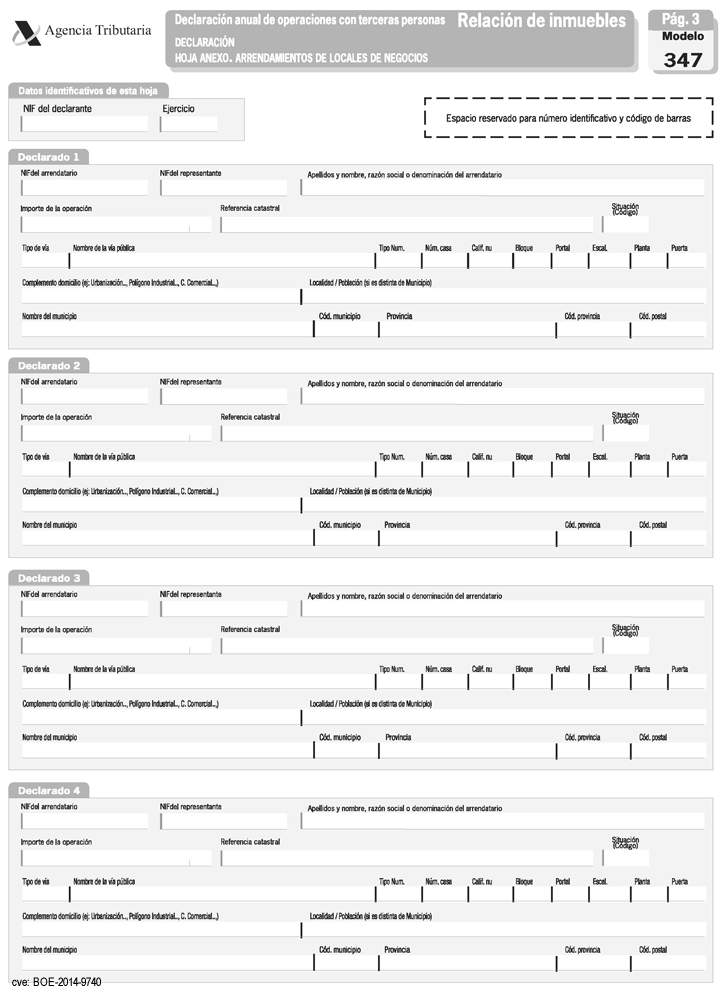

En la tercera página, deberá ser rellenada exclusivamente por los arrendadores de locales de negocio. En ella detallaremos la información de las operaciones de arrendamiento, de los distintos alquileres de locales de negocio u oficinas siempre que el importe anual sea superior a 3.005,06 €.

En cuanto a la situación, insertaremos un “1” para los locales en España (a excepción de Navarra y País Vasco), un “2” para los locales en Navarra y País Vasco, un “3” si no tuvieren referencia catastral y un “4” para los locales fuera de España.

Si no se presenta el modelo 347 se incurrirá en una infracción tributaria, prevista en la Ley General Tributaria 58/2003, siendo ésta una sanción monetaria con un mínimo de 300€ y un máximo de 20.000€.

El modelo 347 permite que la Administración Estatal pueda cruzar información de todo tipo de operaciones. Si se detectaran posibles diferencias, puede iniciarse un procedimiento de inspección. Es por eso que es recomendable contrastar el volumen de operaciones e importe con tus clientes y proveedores.